Pre-Tax vs Post-Tax Deductions: Boost Your Take-Home

TL;DR (Quick Wins)

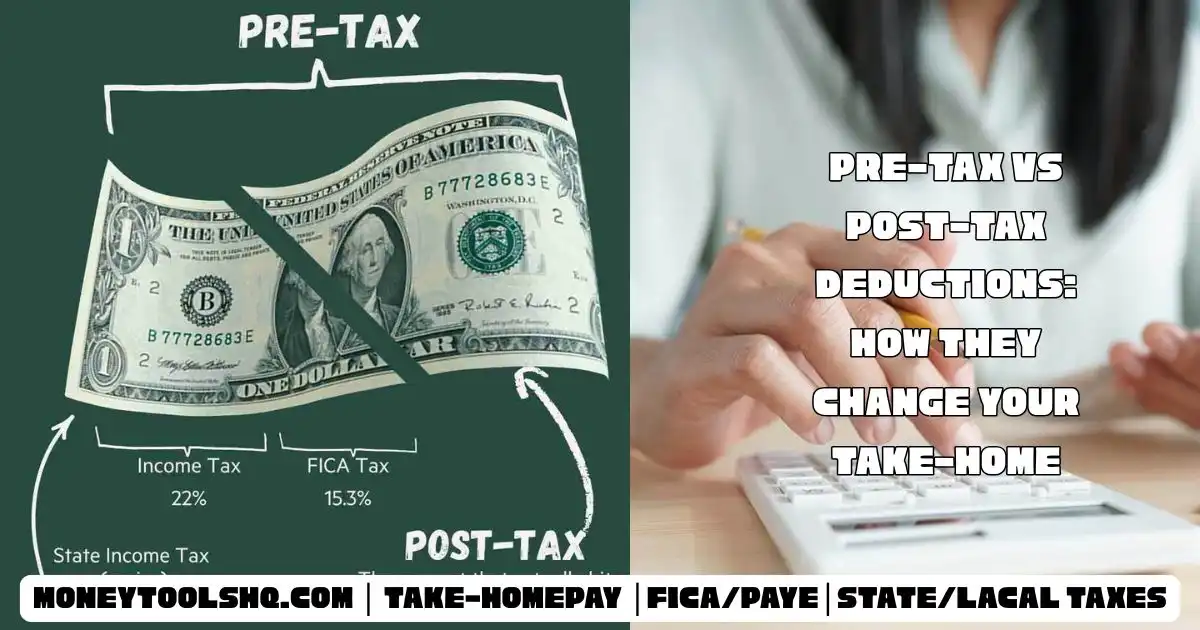

- Pre-tax lowers taxable pay before income tax (and often FICA), raising net pay today.

- Post-tax (e.g., Roth) doesn’t lower today’s taxes but can deliver tax-free withdrawals later.

- 401(k): pre-tax for income tax (not FICA).

- HSA/FSA/Commuter (via cafeteria plan): typically pre-tax for income tax + FICA.

- Impact by bracket: Higher bracket ⇒ bigger pre-tax savings on each dollar.

- Action: Toggle deductions in the calculator to see your take-home change instantly.

The Big Picture: What “Pre-Tax” and “Post-Tax” Really Mean

Your paycheck is built from gross pay → deductions → taxes → net pay.

- Pre-tax deductions are subtracted from your gross before calculating federal income tax, and (depending on the benefit) sometimes before FICA (Social Security + Medicare) and state/local income taxes.

- Post-tax deductions are taken after taxes are computed. They don’t reduce today’s taxable income, but they may deliver future tax advantages (e.g., Roth accounts) or other value (insurance premiums, charitable giving, union dues).

Key outcomes:

- Pre-tax makes today’s paycheck bigger than post-tax for the same dollar contributed.

- Post-tax (Roth) can make future withdrawals tax-free, which is powerful if you expect higher tax rates later.

How Payroll Taxes Stack

- Federal income tax: Progressive brackets (higher slices of income taxed at higher rates).

- State/local income tax: Varies by location.

- FICA:

- Social Security: 6.2% (employee share) up to the annual wage base.

- Medicare: 1.45% (employee share) on all wages; additional 0.9% above a high-income threshold.

Rule of thumb:

- 401(k) deferrals reduce federal and most state income taxes, but do not reduce FICA.

- HSA/FSA/Commuter (Section 125/132 plans) typically reduce federal + state income taxes and FICA (if within limits and under the Social Security wage cap).

- Some states treat HSAs differently; always check your location in the calculator.

Why Brackets Matter (and How to Use Them)

Your marginal bracket is the rate at which your next dollar is taxed. That rate drives the immediate savings from a pre-tax deduction.

For example:

- If your marginal federal bracket is 22%, every $1,000 pre-tax 401(k) deferral saves $220 in federal income tax today (plus any state tax savings).

- If the same $1,000 goes into a pre-tax HSA/FSA/commuter deduction, you typically save income tax + FICA. At 22% federal + 0% state and assuming you’re under the Social Security cap, that’s roughly 22% + 7.65% = 29.65%, or $296.50 saved today.

Dollar Impact by Federal Bracket (No State vs. 5% State)

Below, see approximate “today” savings per $1,000 contributed.

- 401(k): reduces income tax only (federal + state), not FICA.

- HSA/FSA/Commuter: reduces income tax and FICA (assumes 7.65% FICA applies).

- These are illustrative, rounded figures assuming you’re under the Social Security wage cap and that your state conforms to federal rules for the benefit in question.

A) Savings per $1,000 — 401(k) (no FICA savings)

| Federal Bracket | State 0% | State 5% |

|---|---|---|

| 12% | $120 | $170 |

| 22% | $220 | $270 |

| 24% | $240 | $290 |

| 32% | $320 | $370 |

| 35% | $350 | $400 |

| 37% | $370 | $420 |

How to read it: At a 22% bracket and 5% state, a $1,000 401(k) deferral raises your take-home by about $270 today.

B) Savings per $1,000 — HSA, FSA, Commuter (income tax + FICA)

Assumes you’re under the Social Security wage cap and contributions are pre-tax for both income tax and FICA.

| Federal Bracket | State 0% (adds 7.65% FICA) | State 5% (adds 7.65% FICA) |

|---|---|---|

| 12% | $196.50 | $246.50 |

| 22% | $296.50 | $346.50 |

| 24% | $316.50 | $366.50 |

| 32% | $396.50 | $446.50 |

| 35% | $426.50 | $476.50 |

| 37% | $446.50 | $496.50 |

Takeaway: The same $1,000 produces larger immediate savings in HSA/FSA/commuter than in a 401(k) because FICA is included.

Try it yourself: Toggle deductions in the calculator (401(k), HSA, FSA, commuter) and watch your net pay change instantly at different income levels.

Pre-Tax vs Post-Tax: Side-by-Side

| Feature | Pre-Tax (e.g., 401(k), HSA/FSA/Commuter) | Post-Tax (e.g., Roth 401(k), Roth IRA, after-tax benefits) |

|---|---|---|

| Lowers federal income tax today | ✅ | ❌ |

| Lowers FICA today | HSA/FSA/Commuter often ✅; 401(k) ❌ | ❌ |

| Lowers state/local today | Often ✅ (varies by state) | ❌ |

| Future taxation | 401(k): taxable; HSA: tax-free medical; FSA: use-it-or-lose-it; Commuter: n/a | Roth: tax-free qualified withdrawals |

| Best when | You want higher take-home now and/or expect lower retirement tax rates | You expect higher tax rates later or value tax-free retirement income |

| Cash-flow impact | Improves net pay for same $ contribution | Reduces net pay more today for same $ contribution |

401(k): Income-Tax Only (Today), Taxed Later

What it does today:

- Lowers federal and usually state taxable wages.

- No reduction to FICA wages.

Why it matters:

- Immediate savings = Contribution × (Federal bracket + State rate).

- Example: At a 24% federal bracket and 5% state, each $1,000 saves about $290 today.

Later:

- Traditional 401(k) withdrawals are taxable as ordinary income in retirement.

- Consider how your future tax rate compares to today’s.

HSA: Triple Tax Advantage (and Usually FICA Savings)

HSA via payroll typically reduces federal + state income taxes and FICA.

- Immediate savings are often the highest among mainstream benefits because FICA applies.

- Later perks: tax-free growth and tax-free withdrawals for qualified medical expenses—now or decades later.

Strategy:

- If eligible, many planners prioritize HSA payroll deductions (up to IRS limits), then 401(k).

FSA: Health & Dependent Care, With FICA Savings

Health FSA and Limited-Purpose FSA (for dental/vision with an HSA) are usually pre-tax for income tax + FICA.

- Use-it-or-lose-it rules apply (with small carryover/ grace options).

- Great for predictable expenses (braces, contacts, copays).

Dependent Care FSA: pre-tax for eligible child/elder care costs, subject to annual limits and coordination with credits.

Commuter Benefits: Transit & Parking (Monthly Limits)

Transit/parking under IRC §132(f) are typically pre-tax for income tax + FICA, up to monthly caps.

- If you spend, say, $300/month on a metro pass, pre-tax election can save hundreds per year, especially at higher brackets.

Post-Tax (Roth): Max Flexibility Later, Less Cash Today

Roth 401(k)/Roth IRA contributions are post-tax.

- No today savings; net pay drops by the full contribution amount.

- The trade: tax-free growth and tax-free qualified withdrawals later.

- Powerful if you expect to be in a higher tax bracket in retirement, anticipate big investment growth, or value tax diversification.

Case Studies: The $ Impact on Take-Home

Below are simple, round-number examples assuming:

- Under Social Security wage cap.

- State tax row shown at 0% and 5% for reference.

- We only model federal bracket + optional 5% state + FICA when applicable.

- Actual withholding uses IRS tables, credits, and filing details; use the calculator for your precise numbers.

Case 1: $60,000 salary, 22% federal bracket

Scenario A — Contribute $300/mo to 401(k) (pre-tax for income tax only)

- Annual contribution: $3,600

- Savings (State 0%): $3,600 × 22% = $792/yr (~$66/mo higher take-home vs. post-tax)

- Savings (State 5%): $3,600 × (22%+5%) = $972/yr (~$81/mo)

Scenario B — Contribute $300/mo to HSA via payroll (pre-tax income tax + FICA)

- Savings (State 0%): $3,600 × (22%+7.65%) = $1,071.

- Savings (State 5%): $3,600 × (22%+5%+7.65%) = $1,251.

- That’s roughly $90–$104 more per month in take-home vs making the same $300 post-tax.

Scenario C — $300/mo Roth 401(k) (post-tax)

- No immediate tax savings.

- Net pay drops the full $300/mo vs gross.

Tip: If cash flow is tight, shift some dollars from Roth to pre-tax HSA/FSA/commuter to reclaim FICA + income tax savings today.

Case 2: $100,000 salary, 24% federal bracket

$500/mo to 401(k)

- Savings (0% state): $6,000 × 24% = $1,440/yr (~$120/mo).

- Savings (5% state): $6,000 × 29% = $1,740/yr (~$145/mo).

$500/mo to HSA/FSA/commuter

- Savings (0% state): $6,000 × (24%+7.65%) = $1,881/yr (~$157/mo).

- Savings (5% state): $6,000 × (24%+5%+7.65%) = $2,181/yr (~$182/mo).

$500/mo to Roth 401(k)

- No immediate savings; net drops ~$500/mo.

Case 3: $180,000 salary, 32% federal bracket

Assume still under Social Security cap part of the year; once you pass it, FICA savings shrink to just Medicare 1.45% for the remainder.

$1,000/mo to 401(k)

- Savings (0% state): $12,000 × 32% = $3,840/yr.

- Savings (5% state): $12,000 × 37% = $4,440/yr.

$1,000/mo to HSA/Commuter

- Early-year savings with full FICA: $12,000 × (32%+7.65%) = $4,740/yr (~before SS cap is reached).

- After you pass the SS cap, applying only 1.45% Medicare for remaining months lowers total annual FICA savings.

- Use the calculator to pattern this month-by-month with your actual pay schedule.

$1,000/mo to Roth 401(k)

- No immediate savings; future withdrawals tax-free if qualified.

The FICA Twist: Why HSA/FSA/Commuter Often Win “Today”

Because HSA/FSA/commuter typically reduce FICA in addition to income tax, your take-home pay increases more per dollar than a 401(k) does. Two important nuances:

- Social Security wage cap: Once you cross it, the 6.2% piece disappears for the rest of the year, so new cafeteria-plan deductions save only 1.45% Medicare on the FICA side.

- Plan eligibility and limits: HSA requires a qualified High-Deductible Health Plan. FSAs and commuter benefits have annual or monthly caps.

Action: In the calculator, enter your year-to-date wages to accurately reflect whether you’ve hit the Social Security cap.

State Taxes: Why Location Changes the Answer

- Many states mirror federal rules for pre-tax benefits.

- Some do not conform fully (e.g., certain states historically taxed HSAs).

- Commuter and FSA rules can also vary in state treatment.

What to do:

Use the calculator’s state selector. Then toggle benefits and compare net pay for your city/state combination.

Post-Tax With a Purpose: When Roth Is the Right Call

Choose Roth when:

- You expect higher tax rates later (career trajectory, future law changes).

- You value tax-free retirement income flexibility.

- You’re earlier in your career in a lower bracket now.

- You plan to contribute for many years and expect significant growth.

Blended strategy:

- Fund HSA first (if eligible), because it often beats everything for today’s savings and future tax benefits.

- Split 401(k) between pre-tax and Roth to diversify tax exposure.

- Use FSAs for predictable expenses and commuter if you have eligible costs.

Optimizing Order: A Practical Contribution Stack

- Employer match (401(k)): always capture the full match first—free money.

- HSA via payroll (if eligible): typically top immediate tax value + long-term flexibility.

- FSA/Commuter: if you have predictable medical or transit/parking costs.

- 401(k) pre-tax vs Roth:

- Higher bracket today or need higher take-home? Favor pre-tax.

- Expect higher future rates or need tax-free retirement income? Favor Roth.

- IRAs and other savings once workplace plans are maximized.

Common Mistakes (and Quick Fixes)

- Ignoring FICA: Assuming 401(k) lowers FICA—it doesn’t. Use HSA/FSA/commuter for FICA-inclusive savings.

- Forgetting the wage cap: Modeling FICA savings the same all year. Adjust for when you cross the Social Security wage base.

- Over-funding FSA: Not using funds and losing them. Estimate conservatively unless your plan allows carryover.

- Skipping HSA payroll route: Contributing post-tax and deducting at tax time can miss FICA savings. Payroll deductions usually win.

- Neglecting state rules: Assuming federal treatment applies in your state. Always check state impact in the calculator.

- Chasing deductions without the budget: If cash is tight, start with high-impact, low-risk amounts and scale up.

How to Compare in Seconds (Your Workflow)

- Open the paycheck calculator.

- Enter gross pay, pay frequency, filing status, allowances/credits, and state/city.

- Add a 401(k) amount and note your new net pay.

- Zero out 401(k), add the same amount to HSA (or FSA or Commuter).

- Compare nets. The bigger immediate lift in take-home reveals the stronger today benefit.

- Add a Roth 401(k) amount to see the cash-flow trade-off for future tax-free withdrawals.

- Fine-tune the mix until you hit your target take-home and annual savings goals.

CTA: Toggle deductions in the calculator to compare 401(k), HSA, FSA, and commuter benefits for your bracket and state.

Advanced Notes for Power Users

- Medicare Additional Tax (0.9%): Doesn’t change your marginal savings from pre-tax payroll deductions directly unless your wages cross the threshold; the calculator will handle this.

- Local taxes: Some municipalities have wage taxes; these typically follow state-like logic. Toggle city when available.

- Roth conversions later: Doing more pre-tax today and converting in lower-income years can simulate Roth benefits at a lower cost.

- IRMAA & ACA ripple effects: Reducing MAGI via pre-tax can improve next-year Medicare premiums or current-year ACA subsidy eligibility.

- Social Security benefits math: Lower FICA wages (e.g., through cafeteria plans) could slightly reduce lifetime SS benefits; effect is often minimal but real over decades. Balance near-term savings with long-term benefit formulas.

Worked Examples by Bracket (Per $100)

Sometimes it’s easier to think in $100 increments. Below, approximate today savings per $100 contributed:

401(k) (income-tax only):

- 12% bracket: $12 (state 5%: $17)

- 22%: $22 (state 5%: $27)

- 24%: $24 (state 5%: $29)

- 32%: $32 (state 5%: $37)

- 35%: $35 (state 5%: $40)

- 37%: $37 (state 5%: $42)

HSA/FSA/Commuter (income-tax + FICA 7.65%):

- 12%: $19.65 (state 5%: $24.65)

- 22%: $29.65 (state 5%: $34.65)

- 24%: $31.65 (state 5%: $36.65)

- 32%: $39.65 (state 5%: $44.65)

- 35%: $42.65 (state 5%: $47.65)

- 37%: $44.65 (state 5%: $49.65)

Roth (post-tax):

- $0 immediate savings (but future withdrawals can be tax-free).

Choosing Your Mix: Practical Blueprints

Cash-Flow First (maximize take-home today)

- HSA via payroll to the level you’ll actually spend (or fully fund if you can).

- Transit/parking pre-tax up to your monthly need.

- Health FSA for predictable costs.

- 401(k) pre-tax for the rest (capture match first).

Tax-Free Later (prioritize Roth)

- Capture 401(k) match (pre-tax or Roth—match is always pre-tax when it vests).

- HSA via payroll (still hard to beat).

- Shift a meaningful slice of your 401(k) to Roth, especially if you’re in a lower bracket now.

- Keep an eye on IRMAA/ACA thresholds if applicable.

Balanced (hedge future tax uncertainty)

- HSA via payroll.

- Split 401(k) 50/50 pre-tax/Roth (or 60/40) and revisit annually.

- Use FSAs/commuter only to the level you’re certain to use.

Annual Limits, Eligibility & Administration (At a Glance)

- 401(k): Annual employee deferral limit; employer match doesn’t count toward that employee limit but counts toward overall plan limit.

- HSA: Requires a qualified HDHP; separate limits for self vs family; catch-up allowed at a certain age.

- FSAs: Health FSA and Dependent Care FSA each have distinct annual limits; check carryover vs grace-period rules.

- Commuter: Monthly caps for transit and parking; elections can often be changed monthly.

- Roth IRA: Income limits may restrict direct contributions; “backdoor” strategies exist—seek qualified guidance.

- State/local rules: Confirm conformity for HSAs/FSAs/commuter; the calculator’s state setting helps model this.

FAQ:

Q1: I want to contribute $500/mo somewhere. Where should it go?

Start with employer match, then HSA via payroll if eligible. If you commute by transit/parking, add commuter up to your need. With the remainder, decide between pre-tax 401(k) (bigger paycheck today) or Roth 401(k) (tax-free later). Toggle in the calculator to hit your target net pay.

Q2: Does 401(k) reduce FICA?

No. Traditional 401(k) deferrals reduce income taxes today, not FICA. That’s why HSA/FSA/commuter often produce larger immediate take-home increases per dollar.

Q3: Are HSAs always state tax-free?

Not always. Some states diverge. Use the state selector and check the impact in your scenario.

Q4: I’m close to the Social Security wage cap—should I still do HSA/commuter?

Yes, but understand that once you pass the cap, only Medicare (1.45%) FICA savings remain. Your annual savings will still be solid, just a little smaller in later months.

Q5: Is Roth always worse for take-home?

Yes, today. But Roth can be better overall if your future tax rate is higher or you value tax-free retirement income. It’s a strategic trade-off.

Q6: What about after-tax 401(k) (non-Roth) contributions?

Some plans allow them, enabling mega backdoor Roth conversions. This can be powerful but is plan-specific and nuanced—check your plan and model in the calculator.

Implementation Checklist (5 Minutes)

- Enter your paycheck details (gross, frequency, filing status, state/city).

- Add employer match and set initial 401(k) amount.

- Toggle HSA/FSA/commuter to mirror real costs.

- Adjust pre-tax vs Roth until your net pay matches your budget.

- Save the setup and revisit each time your pay or benefits change.

Action: Toggle deductions in the calculator to compare—see precisely how $100, $300, or $1,000/month shifts your take-home across 401(k), HSA, FSA, and commuter.

Bottom Line

- Pre-tax boosts take-home today—especially HSA/FSA/commuter because they usually reduce FICA too.

- 401(k) is excellent for income-tax reduction now, but remember it doesn’t touch FICA.

- Roth sacrifices today’s net for tax-free retirement income, which can be better if you expect higher future tax rates or big investment growth.

- There is no one-size-fits-all answer—your bracket, state, commute, health plan, and wage cap timing all matter.

- The fastest way to the right answer is to toggle deductions in the calculator and compare your own numbers.

Editor’s Note for Power Savers

If you can, aim to:

- Capture the full 401(k) match.

- Max HSA if eligible.

- Use commuter for real costs (don’t over-elect).

- Allocate the rest between pre-tax and Roth to balance today’s cash flow with tomorrow’s tax-free income.

Next step: Open the calculator and toggle your deductions. Your best mix will reveal itself in the net pay line.